Corporate venture capital is a growing trend. Today 71% of the Fortune 100 have corporate venture initiatives (vs. just 10% in 2000) and there are about 1K active corporate venture capital funds (or CVCs) globally. CVC-backed deal volume has increased 10x in the past decade.

All that being said, I heard only vaguely of CVC during my VC recruiting journey. The mainstream of VC recruiting content, resources, and events focus on traditional VC — but there is a ton of value in the CVC space as I’ve learned after just a few months in it myself. In this post, I’ll share more about what CVC is and what it’s like to work within it for the benefit of aspiring VCs and founders alike. Read on for more info!

What is Corporate Venture Capital (CVC)?

A CVC makes venture investments on behalf of a company. CVCs invest in startups to drive innovation at their companies and bring them along on the latest and greatest tech trends, typically investing in areas relevant to their company’s products or services.

CVCs are known as strategic investors for a number of reasons. For one thing, a CVC investment is a good show of confidence, helps legitimize the product, and lends its brand to the startup. There’s also the potential for the company to be a customer of the product and/or help in distribution channels (though an investment doesn’t always guarantee this).

There are many flavors to CVC and every company runs them differently. It all comes back to what the goal of the program is and how it’s structured, but here are a few of the differences I’ve seen so far (and if you’d like to learn more, SVB published a fantastic State of CVC report in 2022):

- Strategic vs financial return: about ~50% of CVCs invest for strategic relevance as well as financial return though ~20% invest purely for financial return and the remaining ~30% invest just for strategic relevance. CVCs who invest for financial return are more likely to lead rounds, though the lead vs follow-on distinction varies by CVC.

- Stage: CVCs primarily invest in mid to growth-stage startups, with 68% of firms targeting Series A and B (e.g. Intuit Ventures and Verizon Ventures). A healthy amount, 19%, are stage agnostic (e.g. AXA Ventures and Amex Ventures) while just 5% focus on pre-seed and seed deals (e.g. Gradient Ventures, CVS Ventures, and Nationwide Ventures).

- Fundraising: CVCs in general invest the company’s money from the balance sheet into startups. However, some CVCs do raise money from LPs and operate in a separate manner while retaining a loose affiliation with the company (e.g. Google is the only LP in GV, which operates separately). There are also CVC/traditional fund hybrids — traditional VC funds that structure their sourcing/diligence around relevance to LPs who are large companies (e.g. Pruven Capital and Illuminate Financial).

- Place within the organization: CVCs can sit within Corporate Development, M&A, Research & Development, Strategy, or Innovation groups among others. Knowing where a CVC sits within an organization will give you good intel into the purpose of the program/how it’s structured.

- Engagement with the business: some CVCs, and especially the ones focused purely on strategic value, require engagement or even sponsorship from a business unit before making an investment. Others make investments independent of the business. This type of information is rarely on the website so you’ll only really know by talking to someone at the CVC.

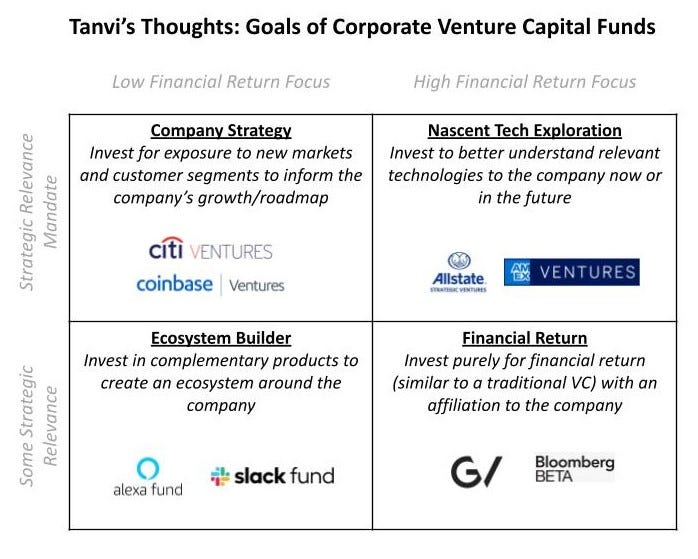

At the end of the day, to really understand CVC you have to go fund by fund. Every program is structured differently and it all comes back to the rationale for launching the CVC programs. To help summarize, here’s a framework I put together combining perspectives from Harvard Business Review and TechNexus:

Aspiring VCs: What to know about CVCs

Someone once told me they wanted to work in CVC because they had heard it was an easier path to break into VC vs a traditional fund. This is simply incorrect so let’s start there. CVC is a different variant of venture capital but requires the same skills and network that a traditional VC role does. In this section, I’ll get into what it’s like to actually work in CVC but if you’re looking for VC recruiting tips make sure to check out my VC Recruiting blog posts.

My day-to-day in a CVC looks the same as other VCs — it’s a mix of sourcing, pitch calls, due diligence, fund administration, and thesis-building work. However, here are a few key differences:

- Types of investments: in addition to direct investments in startups, 55% of CVCs do LP/fund-to-fund investments as well as secondaries. In your role at a CVC, you’ll likely do a mix of all these investments vs. just direct investments.

- Fundraising: in a CVC role, there’s usually no fundraising or LP management. Where many traditional VC firms will spend a large chunk of time on fundraising or have specific personnel dedicated to these activities, this won’t be a part of the job if the CVC invests off the company’s balance sheet (and again, not all do).

- Internal work: on the flip side, as a CVC you’ll need to do internal work to demonstrate your value to the firm — e.g. an insights deck, materials summarizing how you’ve helped drive innovation to the business, etc. Different teams within the business may also pull you into specific discussions where it’s helpful to have someone who’s in the know on all things startup and innovation.

- Navigating a large organization: this is a key skill needed to be successful in CVC, and in particular if the CVC has any kind of strategic relevance mandate. Whereas in a traditional VC this skill isn’t as important, to be successful in a CVC role you’ll need to figure out the right folks in the business to stay in touch with.

I’ve found a lot of benefits to working at a CVC — not having to fundraise, exposure to different types of investments, etc. But there are other, almost intangible benefits that I don’t see online and haven’t heard in conversations:

- You’re joining an existing brand: joining a CVC also means joining a brand that’s already been built over years or decades vs working to build one up at a traditional VC fund. This makes a huge difference in terms of your access and network — founders are almost always willing to take a call with you and/or open up allocation for you in rounds given the potential to collaborate.

- You’re positioned to create value: it’s always an exciting feeling when you connect a startup with an internal PM who’s interested to learn more and potentially get into a proof-of-concept with them. Even if your team doesn’t make the investment — you’ve created value on both sides.

- You have clearly structured performance management processes: this is huge in my opinion. Talent processes tend to be highly opaque, undefined, and inconsistent within traditional VC firms so when you’re in a CVC it’s nice to have that structure and visibility. Larger companies tend to invest more resources into talent processes and company culture so hopefully you’ll see that difference in a CVC as well.

- You have access to shared resources: it’s awesome to have HR, Legal, etc. resources who are there to help and support you in diligence, hiring, and other things. For example, I’m learning a ton from my legal counterpart on what to look for in diligence from their lens.

At the same time, nothing’s perfect — and just as working at a traditional VC comes with its trade-offs so too does working at a CVC. Here’s the flip side of things:

- Limitations in investing themes: most CVCs have some kind of strategic mandate, so as a CVC you’re limited to investing in themes of relevance to the company (vs for example a generalist fund). In my opinion, this is comparable to the traditional VCs that have clear focus areas — but traditional VC funds are also more likely to make one-off investments (either through their fund or an SPV) that a CVC wouldn't.

- Explaining venture to the business: working in CVC is a funny line to dance at times. The learnings and/or financial return from startup investments only kick in after a few years — but the business wants the results now to inform their strategy! Unless the head of the group the CVC reports into has previously been a VC (highly unlikely), there’s a certain navigation required in a CVC to explain what’s feasible and not in the current moment.

- Overlap between the business & startups: as a CVC you have to make sure you don’t invest in a startup that’s directly competing with your company. You can do your best to connect with the business to verify a startup isn’t directly competitive but you can never have insight into every single product roadmap or control what features product teams decide to build in the next year or five years. It can be a bummer to find a deal you really like only to realize this is on the roadmap for the next year. The company will always prioritize its own product above partnerships or investments after all.

Founders: What to know about CVCs

I get a lot of inbound requests to chat from startups and warm intros from my network to startups who want to partner with Intuit. Sometimes there’s an investment opportunity into their round but most times they just want to chat and see if I can introduce them to someone internally for a partnership.

The first thing to say here is that CVCs are investors. Our full-time role is not business development or liaising with the business — it’s making quality investments in startups. While I’m happy to try and connect startups to the teams I know, this is not my entire job. It is always off-putting to have a highly transactional call where founders see me as a stepping stone rather than an investor.

So with that being said — if you’re a founder, here are some thoughts about engaging with CVC investors for partnerships:

- Come to the call with a perspective on what a partnership could look like. Oftentimes startups will just share how Intuit’s products could help them as a distribution channel for customer acquisition. This is a fair thought — but what’s the value back to Intuit? The best calls I’ve had with founders are where they pitch how their product helps Intuit and/or share interesting learnings about how customers are using our own products.

- Remember that the CVC doesn’t control the business’s focus or roadmap. We can make the introduction and share what we know — but at the end of the day it’s on you to close the deal and navigate the sales process.

- If you’re an early-stage founder make sure you have traction and some prior successes before pitching a partnership to a CVC. A pre-seed or seed stage startup is rarely ready for an enterprise customer and I am not sure if many of the early-stage founders I speak with are mature enough to work with an enterprise product team.

- If you’re actively raising for a round — ask what their diligence process looks like. Every CVC is different and it’s important to know, for example, if they require BU sponsorship, what their legal diligence looks like, how long they typically take to make an investment, etc. I’d also recommend asking how partnerships with their portfolio companies work and if/how the CVC helps facilitate that (this too will vary by CVC).

For all the CVC-curious — I hope this helps! What else would you like to know about CVC? What other types of CVCs have you seen? Leave me a comment and don’t forget to follow me on Twitter & LinkedIn!